Introduction

Over the past decade, abuses by colleges operating in the for-profit education sector have been well documented.1 Buoyed by a tide of government-enabled financing, these for-profit colleges expanded their enrollment from 1990 to 2013 more than ten times faster than did nonprofit or public schools,2 and they widely engaged in aggressive and misleading recruitment and other predatory practices3—all to fill programs that had abysmally low completion and job placement rates. Many students that had enrolled in for-profit colleges were left with huge student loan debts and little else to show for their education investment. Meanwhile, taxpayers shelled out billions of dollars in financing and tax breaks for these schools, with little accountability to ensure that their students were getting an education that would lead to gainful employment.

Today, many of these for-profit institutions find themselves on the defensive and are now being scrutinized more closely, both by the government agencies that finance them and by consumers who may seek, instead, to enroll at public and other nonprofit institutions. High-profit, high-enrollment schools such as ITT Tech, DeVry, and the University of Phoenix are allowed to continue to participate in the federal loan program, but under even stricter rules.4

Recently, a new trend in the abuse of college students and federal education dollars may be under way: the creation of the covert for-profit. The owners of some for-profit institutions have sought to switch their schools to nonprofit status, freeing them from the regulatory burdens of for-profit colleges, while continuing to reap the personal financial benefits of for-profit ownership.

Prompted by news of several recent conversions of for-profit colleges into nonprofits, The Century Foundation has obtained IRS and U.S. Department of Education records and communications that call into question the legitimacy of some of these conversions. Through four case studies, based on hundreds of pages of documents obtained from government agencies, the examination reveals a dangerous regulatory blind spot, with the two federal agencies each assuming, wrongly, that the other is monitoring the integrity of the “nonprofit” claims of these colleges.

This report begins by describing the role of nonprofit governance in promoting good stewardship in education and the problems that have resulted from unrestrained profit-seeking in American higher education. The case studies then lay out four instances of possible covert for-profits, where owners have managed to affix a nonprofit label to their colleges while engineering substantial ongoing personal financial benefits for themselves. The report concludes with specific steps government regulators should take to prevent illegitimate claims to nonprofit status and to protect students and the public interest.

The Public Trust Purpose of Nonprofits

An enterprise organizes itself as “nonprofit” to provide some assurance to customers and donors that while the organization needs money to pursue its mission, the ultimate goal is not financial. Two core requirements are designed to offer that assurance. First, anyone who is paid is, ultimately, answerable to someone who is not. Those unpaid overseers are often called “trustees” because they are entrusted with the responsibility of ensuring that the organization is pursuing a charitable or educational goal rather than simply financial gain. They are unpaid (except in special circumstances) so that their judgment of what is best for students or society is not skewed by a personal financial interest. Second, any money that is earned by the organization beyond what is needed to pay expenses (the amounts that would be profit in a for-profit entity) is reinvested in the organization. In other words, no one owns stock or shares that can be sold or earn dividends. The trustees control the organization in the same way that owners would, but they cannot take the money for themselves.5

Nonprofits are common in ventures that involve goals that are difficult to measure or populations that are vulnerable, such as public health, caring for the poor, the arts, religious or spiritual fulfillment—and education. In return for serving society’s interests above private interests, nonprofit organizations are favored in providing certain types of services and are granted tax exemptions that can be substantial.

The unpaid trustees are seen as such a bulwark against abuse that the organizations are, in some cases, allowed to engage in practices that would be illegal in a for-profit context. Many nonprofits, for example, involve vast numbers of people who work for free as volunteers, a practice that is highly restricted in the for-profit environment. Imagine a supermarket or snack food chain enlisting two million underage girls to sell cookies: the operation would be shut down and the companies would be prosecuted. Yet the nonprofit Girl Scouts do exactly that every year, selling 175 million overpriced cookies baked by for-profit contractor bakeries. This “child labor” is not illegal because the Girl Scouts councils are nonprofit: their unpaid boards are trusted to engage in this cookie selling, which they believe benefits the girls and is consistent with the values of the organization. Compared to the supermarket owner or cookie baker, the Girl Scout councils are far more likely to make decisions that truly benefit the girls—because council members do not have a personal financial interest. They are not allowed to keep the money for themselves.

The nonprofit organization that runs Wikipedia offers a different type of example of how being a nonprofit affects the decisions that are made. While Facebook, Google, and other investor-owned Internet companies have all decided to take and sell our personal data for profit, Wikipedia has, remarkably, respected users’ anonymity. Wall Street types, salivating over Wikipedia’s billions of page views and massive troves of salable user data, think the people who run the organization are completely nuts. One analyst detailed all of the ways that Wikipedia could earn money, from selling advertisements to t-shirts, and calculated the website’s lost revenue at $2.8 billion a year—forty-six times the organization’s current income.6

Who would leave that kind of money on the table? People who are not allowed to take it. If Wikipedia had owners instead of trustees, the temptation to grab nearly $3 billion would be impossible to resist, even though it would destroy Wikipedia as we know it. Instead, Wikipedia has kept consumers’ interests at the forefront because it is a nonprofit organization. It is a different beast as a result of being structured without owner-investors.

Putting non-owners in control serves as an internal regulatory mechanism, muting the temptation to “cut corners on quality or otherwise take advantage of user vulnerability,” economists say. As a result, nonprofits “are more immune against moral hazards than for-profit firms would be under similar circumstances.”7

For-Profit Ownership’s Bad History in Higher Education

In many contexts, a for-profit business structure operates beautifully, almost miraculously, leading to positive outcomes for provider and consumer alike. In education, however, because of the nature of the goal and “customer” (both students and society), the results of for-profit provision have frequently proved one-sided. The ability of investors to pocket whatever (often taxpayer-supplied) funds that are not already spent, or to buy and sell shares in the business organization, can prompt noticeably different choices on a range of institutional decision points, such as:

- Which students to recruit and enroll; whether to enroll students who are on the borderline of academic qualifications.

- Whether and how fast to grow enrollment, given the need to maintain quality.

- How much to charge which students (pricing and aid/discounts).

- Who to hire as instructors and staff.

- How much to rely on full-time versus adjunct faculty.

- How much to defer to faculty expertise.

- The type of information and advice to provide to potential students.

- Which programs (majors) to create, expand, or contract.

- How standardized the curriculum should be.

- How and where to advertise; what information to put on the website.

- How much to spend on recruitment of applicants.

- What level of student performance is adequate to pass a class or to receive a degree.

At every turn in the educational enterprise, the owner’s profit motive can distort the educational mission, making owner-operated schools more aggressive and singly-focused on maximizing return, even to the point of self-deception. And in fact, the presence of profit in higher education over the years has led to a series of scandals—and resulting attempts at reform.

When the G.I. Bill (the Servicemen’s Readjustment Act of 1944) was enacted for soldiers returning from World War II, the funds they received could be used at any type of school. By 1949, more than five thousand new for-profit schools had sprung up. Investigations revealed that many of the schools were “inflating tuitions, extending the length of courses, enrolling too many students,” and keeping students on the attendance rolls long after they had stopped attending.8 To address the problems, Congress adopted a paying-customer requirement: schools would need to show that someone other than veterans was enrolled so that the schools could not simply price their programs to milk whatever maximum amount taxpayers offered up. It was a market test, called the 85–15 rule because no more than 85 percent of the students in a program could be veterans financed by the government.9

Sobered by the G.I. Bill experience, Congress, when creating the first national student loan program in 1959, restricted funding to public and nonprofit institutions.10 When for-profits were later invited in, it was through what was considered a narrow and limited exception: loans would be available only for job-specific training, leading to “gainful employment in a recognized occupation.”11 Experts had assured Congress that occupational programs were a safe role for schools with owners because the programs would lead to graduates earning “sufficient wages so as to make the concept of student loans to be [repaid] following graduation a reasonable approach to take.”12 Unlike a broader liberal arts education, which is difficult to measure, it would be easy to tell if a for-profit school is not offering valid training for a job.

The narrow vocational exception worked well for a while. But colleges were allowed to self-certify that a particular program was occupational in nature. While a program labeled as Liberal Arts or Philosophy might be rejected by the U.S. Department of Education, in most cases the companies’ assertions were not challenged. As a result, over time, the colleges broadened and extended their offerings while continuing to check the box—declaring that each program “leads to gainful employment in a recognized occupation”—to gain them access to federal grants and loans. The career schools slowly but decidedly started thinking of themselves as no different from public and nonprofit colleges—even though the financial incentives and control structures were different in critically important ways.

In the 1980s, an explosion of student loan defaults led to what President Reagan’s secretary of education William J. Bennett called “shameful and tragic” actions by for-profit institutions, evidence of “serious, and in some cases pervasive, structural problems in the governance, operation, and delivery of postsecondary vocational-technical education.” Releasing a report to Congress about the problem, Bennett said, “The pattern of abuses revealed in these documents is an outrage perpetrated not only on the American taxpayer but, most tragically, upon some of the most disadvantaged, and most vulnerable members of society.” The head of the trade association representing for-profit pledged to work with the secretary and the Congress to “close down any institution that is not operating in an ethical way.”13

The 1980s abuses led Congress to enact a long list of reforms in 1992. Most of the reforms applied to all colleges, whether they had investor-owners or not. One provision that applied to for-profit institutions was a Department of Education version of the G.I. Bill’s paying-customer requirement. Originally 85–15, and later changed to 90–10, it requires schools to show that they are not wholly reliant on money from the Department of Education.

In recent years, problems in federally funded for-profit education have reemerged with the advent of online education, weakened regulations, and lax enforcement. Starting in 2009, the Department of Education took a number of steps to firm up regulations designed to prevent fraud and abuse in the federal financial aid programs. Most of the regulations, such as the ban on bounty-paid recruiters, apply to all types of colleges and programs.

The regulatory proposal that was fought most vigorously by the for-profit lobby was a clarification of what it means to be an occupational program that “prepares students for gainful employment in a recognized occupation.” Offering career-preparation programs is the primary route by which for-profit institutions gain access to federal funds, and the new “gainful employment” rules will end federal funding of programs that consistently fail to bring graduates adequate earnings given the student loan debt they are taking on.14

With the public and regulators increasingly cautious about for-profit education, what are college owners to do?

For-Profit Colleges Hiding in a Regulatory Blind Spot

To escape the gainful employment and 90–10 rules, and to reassure consumers who have become wary of for-profit schools, some large education companies are beginning to explore whether they simply can reclassify themselves as nonprofits.15 A valid and complete conversion—led by trustees with no financial interest and operating in good faith—would provide the oversight that makes nonprofits a better value and less inclined toward predatory practices.

Unfortunately, the conversion to nonprofit status is susceptible to abuse by covert for-profits—schools that obtain the nonprofit label yet continue operating like for-profit institutions—leaving consumers and taxpayers more vulnerable than ever.

Covert for-profit colleges can exist because while the Department of Education relies on the Internal Revenue Service’s judgment of which institutions are and which are not valid nonprofits,16 the IRS rests its determination on the declarations and self-regulation by the trustees of these nonprofits, based mostly on an honor system. As with other taxpayers, the IRS relies on the honesty of the individuals and corporations that file tax returns, an honesty that is tested only in case of an audit, which often takes place years afterward.

The path to nonprofit status starts, of course, with paperwork. Organizations that seek to be designated by the IRS as a tax-exempt nonprofit must complete a Form 1023, which asks a long list of questions about the entity’s goals, structure, management, and finances. Sometimes, an examiner in the IRS Exempt Organizations Division will seek clarifications before designation as a tax-exempt entity is awarded, but the conclusion of the process relies on the assumption that the information provided by the respondent accurately reflects how the organization will wind up operating.

The IRS is quite aware that organizations evolve, sometimes in ways that are contrary to the rules that are supposed to apply to nonprofit entities. Since it would be impossible for the IRS to review and approve the nearly constant changes at the nation’s more than 1,630,000 recognized tax-exempt organizations, the IRS relies on a system of self-regulation, backed up by the threat of potentially retroactive revocation of tax exempt status. For example, when awarded nonprofit status, organizations are told by the IRS that if they change their structures and operations, they do so at their own peril:

A ruling or determination letter recognizing exemption may not be relied upon if there is a material change inconsistent with the exemption in the character, the purpose, or the method of operation of the organization.17

The “IRS determination letter” is not only revocable, it can be revoked retroactively

if the organization omitted or misstated a material fact, operated in a manner materially different from that originally represented, or engaged in a prohibited transaction. . .for the purpose of diverting corpus or income from its exempt purpose.18

The revocation can go back as far as the entity’s original approval as a nonprofit so that an entity that we all thought was a charity can be declared to have never been one. This look-back reparation was tested and affirmed in a seminal case decided in 2013: an organization aimed at helping people make down payments on purchasing homes was found to not be functioning as a valid nonprofit, and the IRS in 2010 revoked its tax-exempt status effective back to the organization’s creation in 2000, ten years earlier.19

Put simply, if an organization acts like a for-profit entity, restructuring or operating in a way that is benefiting a particular person or family, the nonprofit designation can be revoked retroactively by the IRS.

The IRS, however, reexamines less than 1 percent of existing nonprofits each year,20 which means that an entity without the requisite internal checks and balances in place to ensure nonprofit governance can operate in violation of IRS rules for years, or even decades, without getting caught.

Meanwhile, the Department of Education currently relies solely on the IRS label in determining nonprofit status. Beyond the IRS designation, there is no routine effort to ensure that a school is actually following the core expectations of nonprofits.21 Maneuvering to affix a nonprofit label allows a school to essentially hide in plain sight, avoiding the regulations and scrutiny applicable to for-profit colleges as well as the financial accountability required of nonprofits.

Possible Covert For-Profits: Four Case Studies

Government records of four newly designated nonprofit schools that had all previously been operating as for-profit entities reveals some troubling behavior. While IRS Form 1023 filled out by the four college chains undergird the claims that they are making to nonprofit status, the annual tax returns (Form 990) filed by the colleges, and other evidence about the schools’ actual activities and intentions, indicate that three of the four are operating in ways that are not at all consistent with what the organizations asserted when they were seeking the initial IRS approval; the fourth college’s application appears to have gone through the IRS review without detection or discussion of its internal conflicts of interest.

Each year, more than half a billion tax exempt dollars have been flowing to just the four institutions examined for this report: Herzing University; Remington Colleges, Inc.; Everglades College; and the Center for Excellence in Higher Education (CEHE). The findings of this report, however, indicate that their regulatory treatment as nonprofit schools may not be justified.

Herzing University

When Herzing University was profiled in a U.S. Senate report in 2012, it was a privately held, for-profit company headquartered in Milwaukee, Wisconsin, with eleven campuses in eight states. While still relatively small, it had grown by 260 percent since 2001, to more than 8,000 students. Founded in 1965 by Henry and Suzanne Herzing, the company was originally a computer-training institute. Over time, it had morphed into a “university” offering Associate and Bachelor’s degree programs in business management, electronics, health care, graphic design, and public safety, as well as some Master’s degrees (online only). 22

In the 2008–09 school year, Herzing’s federal financial aid revenue grew to $73,633,448, a 42 percent increase over the prior year. At the same time, however, the proportion of revenue coming from paying customers or other sources of financial aid was dropping: 18 percent overall in 2008, 15 percent in 2009, 14 percent in 2010.23 As a result, the school was approaching the 10 percent minimum that is required under the Department of Education’s 90-10 rule. While the company is not allowed to count its own scholarships given to students as part of the 10 percent, support from independent scholarship programs would count.

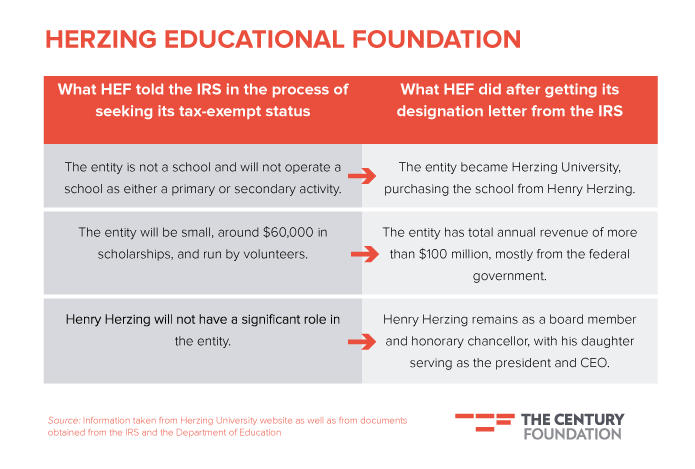

On December 29, 2009, Henry Herzing submitted a Form 1023 to the IRS, seeking a tax-exempt designation for a new corporation called the Herzing Educational Foundation Ltd., which would provide college scholarships to poor students. The application was assigned to specialist Terry Izumi in the Cincinnati, Ohio, office of the IRS. Izumi was skeptical. Normally, giving scholarships to the poor would be a slam-dunk for an organization seeking nonprofit status. But the application was unusual because the scholarships would pay tuition at only one particular school, bearing Henry Herzing’s name. Izumi investigated and discovered that the eponymous college was a business owned by Herzing.

In a letter to Henry Herzing, Izumi explained that, to be considered nonprofit, an organization must demonstrate that “it is not organized or operated for the benefit of private interests,” such as particular individuals, their family members, shareholders, or people controlled—directly or indirectly—by business owners or their family members. Why, Izumi asked, is the board of the Herzing Educational Foundation composed of people who own or operate the for-profit college, rather than by independent members of the community? If the board continues to include people with a financial interest in Herzing University, what system of checks and balances will be used to assure that the assets of the nonprofit are used exclusively for charitable purposes? How does the public know that you are not using the scholarship program as a recruiting tool of the for-profit entity?

After talking with Izumi by phone more than once, Herzing’s lawyer sent to the IRS an eight-page letter, asserting that: (1) the foundation’s day-to-day operations “will be minimal,” with volunteers doing the bulk of the work in administering, perhaps, $60,000 in scholarships; (2) “there is no intent to use the assets of the organization for any other purpose” besides scholarships; and (3) “it is not anticipated that Henry Herzing will have a significant formal voice” in the nonprofit’s activities. Two weeks later the IRS granted the scholarship foundation’s request for status as a public charity. Then, last year, the foundation’s leadership decided to use the nonprofit entity in a very different way (see Table 1).

Table 1

The nonprofit purchased Herzing University for $86 million from the Herzing family, effective January 1, 2015, and continues some leases of property from Herzing family members. According to a press report, a state official said that Herzing likely made the change to avoid new federal regulations and to gain access to state grant funding.24 In response to a request for comment, attorneys for Herzing University (the nonprofit) assert that the purchase price, to be paid over thirty years, and the leases are approved by independent board members at fair market values and that “rigorous conflict-of-interest rules are followed in all such instances.”

After questions were raised about the transaction by this author and by members of Congress, the university on July 6, 2015, asked the IRS to update its classification to reflect that it had become an educational institution. The IRS did so on August 19, noting that it had not undertaken a fresh review of the entity’s nonprofit status. As of September 9, 2015, the Department of Education considers Herzing’s request to be considered a nonprofit an open case “undergoing substantive review.”25

Source Documents for Herzing University

- December 2009 Form 1023 and related materials [Application for Recognition of Exemption under Section 501 (c)(3)]

- IRS Request for Additional Information (August 2010)

- Herzing Response (August 2010)

- IRS Determination Letter (September 2010)

- 2011 Form 990

- 2012 Form 990

Remington Colleges, Inc.

And Educate America

Between the time that the Herzing Educational Foundation submitted its application for tax-exempt status and the actual designation by the IRS, more than eight months had passed, about the average time that it takes for IRS review of a Form 1023. Remington Colleges, Inc., with nineteen campuses in ten states and an online operation, got its IRS designation in eight weeks flat.

At the same time that it sought nonprofit status, Remington Colleges purchased a chain of schools, Educate America, owned primarily by Jerald Barnett, Jr., for $217,500,000. The college was quite open about the fact that it was attempting to evade the 90–10 rule, which requires colleges to show that at least 10 percent of their revenue is from courses other than the U.S. Department of Education. The Chronicle of Higher Education quoted school officials as saying that the reason for becoming nonprofit was to escape the 90–10,26 a U.S. Senate committee’s review of financial data concluded that the school’s difficulties in meeting the 90 percent threshold “likely served as the prime impetus for conversion to nonprofit status,”27 and the school’s application for tax-exempt status actually includes escaping regulations as a reason for becoming nonprofit.28

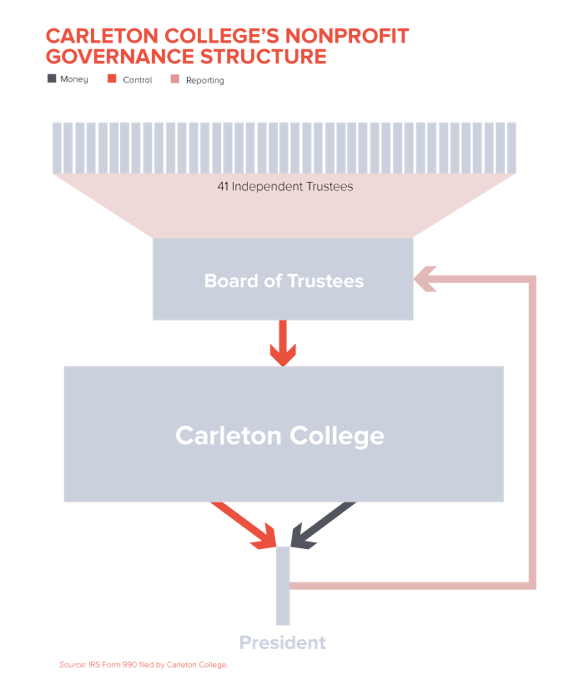

For a nonprofit, however, the structure of Remington Colleges, Inc., is extremely unusual. As described earlier, the board of trustees for a nonprofit is normally comprised of people who care about the organization’s mission but do not gain any financial benefit from it. Carleton College in Minnesota, for example, is controlled by forty-two trustees (see Figure 1). Only one of them, the president of the university (who is hired by the rest of the board), earns anything at all. Everyone else donates time and, likely, money to the college, without the expectation of a financial return on their investment.

Figure 1

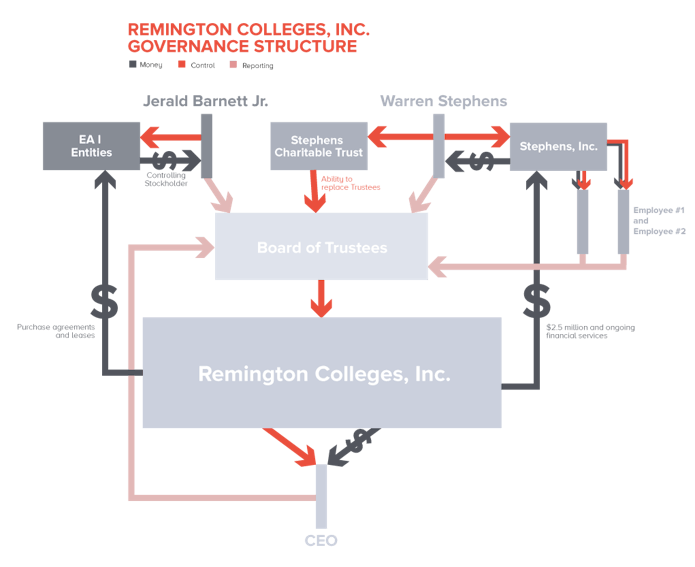

Remington Colleges, in contrast, has a five-member board of trustees. One of them is the CEO of the colleges. Another is the primary creditor, Jerald Barnett, whose company is collecting payments from Remington’s purchase of his Education America campuses and who is the landlord for the properties used by the schools. The three other board members, considered independent in the Remington application for tax-exempt status, are the principal and two employees of a financial services firm, Stephens, Inc., which assisted with the purchase of the Educate America campuses for a fee of $2.5 million. Furthermore, Stephens, Inc., will continue to be paid by Remington to manage the retirement plan for employees (amounts not disclosed). Not only that, but Remington has given Stephens, Inc., an explicit waiver regarding conflicts of interest—meaning that the firm can choose investments that benefit Stephens, Inc., even if the investment choices are bad for Remington Colleges.29 And the Remington board of trustees is actually not even in control. Instead, Warren Stephens, the owner of Stephens, Inc., has the power to replace Remington board members without cause.30

As Figure 2 shows, Remington’s control structure is extremely convoluted, and may lack protections against self-dealing.

Figure 2

How did the IRS miss all of this in the exemption application? The IRS may have rushed because of the requester’s insistence on an expedited review, accompanied with an explanation that created the impression that the U.S. Department of Education needed an answer within a particular time frame, which the lawyers for Remington described as about seven weeks from the date of their application. Among the exhibits submitted by Remington in the 2010 Form 1023 application was the following “Expedite Request”:

—

Re: Remington Colleges, Inc.

EIN: 27-3339369

FORM 1023, EXPEDITE REQUEST

Ladies and Gentlemen:

The transaction is scheduled to close on December 1, 2010. The transaction cannot close unless the College receives a favorable IRS Determination Letter indicating that the College is a qualified §501(c)(3) tax-exempt organization. The necessity of obtaining an expedited determination is magnified by the fact that the College is required to make a change of control filing with the United States Department of Education to obtain approval of the transaction not less than 45 days prior to the closing date in order for the students enrolled in the Schools to continue to be eligible to receive loans and grants under the Title IV federal financial aid programs. The College must submit with the change in control application the IRS Determination Letter on the College indicating that the College is a §501(c)(3) tax-exempt organization. To close by December 1, 2010, would require that the change of control filing be made not later than October 15, 2010.31

—

The application materials provided by the IRS appear to indicate that the Remington application was approved without any questions from the IRS specialist to the applicant, in stark contrast to time and attention that the IRS put into its review of the Herzing application.

Remington officials did not respond to a request for comment from The Century Foundation.

Source Documents for Remington Colleges

- August 2010 Form 1023 and related materials [Application for Recognition of Exemption under Section 501 (c)(3)]

- IRS Determination Letter (October 2010)

- 2012 Form 990

Everglades College

DBA Everglades University and Keiser University

The Form 1023 that Arthur Keiser submitted to the IRS in September 2000 seeking nonprofit status for Everglades College raised suspicions, leading to a twenty-one-month, 388-page tug-of-war between the Everglades lawyers and the IRS. The exchange between Keiser and the IRS is curious in its complexity—the IRS obviously saw many red flags in the application, yet eventually granted the college tax-exempt status. The record of the IRS requests and how Everglades responded to them provides a telling illustration of the principles at stake concerning nonprofit governance.

On March 7, 2000, Arthur Keiser petitioned the Florida Division of Corporations to change the name of a for-profit company he had purchased, American Flyers College, Inc., to Everglades College, Inc., and to convert the entity to a nonprofit corporation under Florida law. On September 6, 2000, Keiser filed a Form 1023 with the IRS seeking federal tax-exempt status for the converted company. The application was assigned to charitable organization specialist Aletha Bolt and then transferred to specialist John Jennewein in Cincinnati.

The IRS had a lot of questions. The first set, sent in a January 2001 letter, included inquiries about a lease agreement between the proposed nonprofit and a company owned by the Keisers, Keiser School, Inc.; details of the purchase of the for-profit predecessor corporation; the assets and liabilities of Everglades and of the Keisers; and an appraisal of the value of the college. Everglades responded.

The IRS asked for more information about compensation of board members, the salaries and qualifications of faculty, and related topics. Everglades responded.

The IRS requested more information including the Keiser purchase agreement, the management agreement between Everglades Management (previously disclosed as owned in part by Keiser) and the college, any loan agreements, and an explanation of the connections to Keiser College, Keiser Career Institute, and Keiser Management Inc., Susan Ziegelhofer, the president of Everglades College, Inc., responded that there was no purchase agreement: the transfer of the college “was a charitable contribution of the entire educational facility.” She further declares that there are no loans between the for-profit and tax-exempt entities.

In response, the IRS requested that Everglades provide the following information regarding loans or payments to Keiser-controlled entities:

For each of the following please explain and specify the accounts:

a. Accounts Payable and Accrued Expenses please provide a detail [sic] explanation why there is a $50,951.18 debit balance in this account?

b. If you have no loan or note agreements who is the loan with and what is the relationship for the Loan Payable of $16,208.41 and please explain the terms and conditions of the loan?

c. Who is the Loans and Notes Receivable with and what is the relationship and please explain the terms and conditions of the loan?

d. Who is the Loan Receivable in the amount of $1,655 with and what is the basis for the loan and please explain the terms and conditions of the Loan Receiveable?

e. Why do you show an amount due to Keiser College for the amount of $463. [sic]

f. If you have no management contracts or fees charged by Everglades Management, Inc explain why do you show an amount of $8,232 due to them? If it is for services please explain the services and what the basis for the charge?

On July 10, 2001, Arthur Keiser, writing as chancellor of Everglades College, explained the various loans and amounts.

On July 16, 2001, a letter from the director of the Exempt Organization Division of the IRS declared the case closed because “we have not received the information necessary to make a determination of your tax-exempt status.”

Months went by, with no documents in the IRS file indicating what, if anything, happened. Then, on December 18, 2001, Jennewein sent to Everglades a detailed seven-page description of the problems with the request for tax-exempt status for Everglades. He cited as reasons for concern the fact that the Memorandum of Understanding for flight training “is serving the private benefit of a for-profit entity” and that “Everglades gave scholarships . . . to students at Keiser College, a for-profit college owned by Arthur, Evelyn, and Robert Keiser.” Therefore, as Jennewein described in his letter, Everglades is serving the private benefit of a for-profit entity,” as well as renting of Keiser-owned buildings:

Correspondence dated March 30, 2001 signed by Arthur Keiser, President of Everglades College, stated that the building in which the school is located is owned by a partnership in which related parties have a 42% interest and unrelated parties owned a 58% interest. The related parties are Keiser Building Corp., which is owned by Arthur Keiser who owns a 2% interest in the partnership; Spectrum Investment Associates which owns a 40% interest in the partnership is owned 48% by Arthur Keiser, 48% by Belinda Keiser and 4% by Robert Keiser. These joint venture (owned 42% by related parties) leases space to Keiser College which in turn’s subleases to Everglades College, Inc. The entire building comprises 83,824 square feet, including the are [sic] occupied by Everglades College. Also, housed in this facility are Keiser Career Institute and Everglades Management Company. Again, this arrangement services the private benefit of the Keisers and they’re related for profit entities.

He cited the laws, regulations, and court cases governing tax-exempt entities, including a case that says:

When a for-profit organization benefits substantially from the manner in which the activities of a related organization are carried on, the latter organization is not operated exclusively for exempt purposes within the meaning of section 501(c)(3), even if it furthers other exempt purposes.32

He cited a school-specific ruling from the IRS that hinges in part on the board of the nonprofit being “completely different” from the for-profit entity’s owners:

Rev. Rul. 76-441, 1976-2 C.B. 147, presents two situations concerning school operations. In the first scenario a nonprofit school succeeded to the assets of a for-profit school. While the former owners were employed in the new school, the board of directors was completely different. The ruling concludes that the transfer did not serve a private interest. Part of that conclusion was based on the independence of the board. In the second scenario, the for-profit school converted to a nonprofit school. The former owners became the new school’s directors. The former owners/new directors benefited financially from the conversion. The ruling concludes that private interest was served. The conclusion is stated as follows: “The directors were, in fact, dealing with themselves and will benefit financially from the transactions. Therefore, (the applicant) is not operated exclusively for educational and charitable purpose and does not quality for exemption from federal income tax under Section 501 (c) (3) of the Code.”

He explained why Everglades does not qualify as tax-exempt, and suggested that the application be withdrawn:

Everglades College is privately held and controlled by the Keisers despite the fact that they do not constitute a majority of the governing board. Therefore, it appears you operate for the benefit of private interests of the Keisers. You are similar to the organization in Old Dominion Box Co. . . . because you operate for the benefit of private parties. Operating for the benefit of the Keisers is a substantial nonexempt purpose that will preclude exemption.

Although Everglades College is offering educational courses to further one career, the central question is whether you operate for the benefit of private interest of designated individuals, or the creator or the creator’s family. In Rev. Rul. 76-441 a for-profit school was converted to a nonprofit school in which former owners/new directors benefited financially from the conversion. The ruling concludes that private interest was served. Although the operation of a school is a charitable activity, the manner in which you operate leads to conclude that your school bestows significant private benefit for the Keisers and their for-profit corporation.

Based on the facts and circumstances provided to date, it appears you cannot satisfy the basic requirements for exemption, in that you fail the operational test. To determine if you qualify under Section 1.501(c) (3)-1 (c) (1) of the regulations the Service determines if the organization engages primarily in activities which accomplish one or more exempt purposes. Section 1.501 (c) (3) – 1 (d) (1) (ii) of the regulations expands on the operated exclusively concept by providing that an organization is not operated exclusively to further exempt purposes unless it serves a public rather than a private interest. Based on the facts that you have provided in your application for recognition of exemption, it appears you are operated for a private purpose rather than a public purpose.

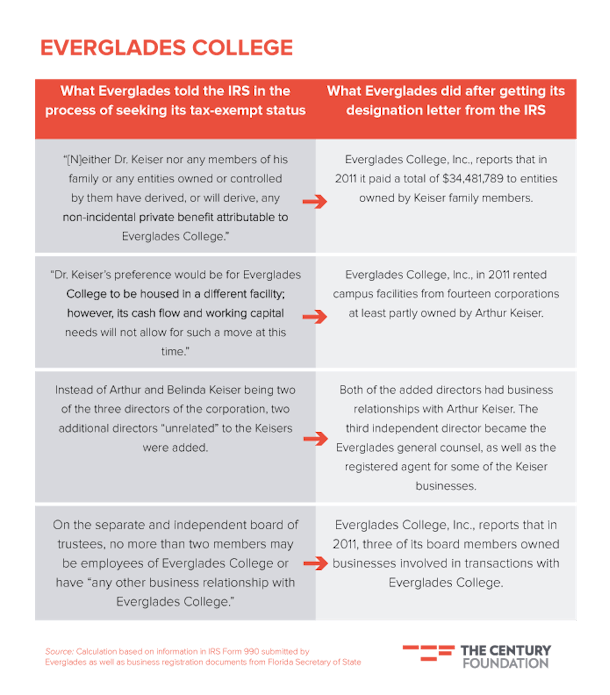

On January 2, 2002, the Everglades attorneys sent a letter, signed also by Arthur Keiser, detailing their responses to the December IRS letter, declaring that the Keiser scholarship recipients “were selected by an independent Board of Trustees”; that the rent paid to the Keisers is at fair market value and that “Dr. Keiser’s preference would be for Everglades College to be housed in a different facility; however, its cash flow and working capital needs will not allow for such a move at this time”; and that the college will actually be run not by the board of directors of the corporation, but by the board of trustees (which includes Chancellor Keiser), which is an “independent governing board.”

The thirteen-page Everglades response asserted multiple times that “Everglades College is governed by an independent Board of Trustees. Dr. Keiser has no control over the Board of Trustees or its decisions.” Responding to the IRS’s concern that Everglades College appears to operate for the benefit of the Keisers, the letter said that the opposite was the case: “now that Keiser College is planning to become a four-year program. . . . Everglades College will actually become a ‘competitor’ to Keiser College.” The letter said at least twice that any benefit to the Keisers from Everglades was incidental at most, and concluded by saying: “Again, let me reiterate that neither Dr. Keiser nor any members of his family or any entities owned or controlled by them have derived, or will derive, any non-incidental private benefit attributable to Everglades College.”

The IRS followed up with a request for more information, such as purchase agreements and details on shared space with Keiser College, asking specifically about the independence of the board of trustees. Everglades responded. The IRS then sent a letter recommending that the board of directors be expanded by two people “selected from the community in which you serve.” Everglades responded by adding two new directors, Dale Chynoweth and Zev Helfer, “who were selected from the community [and] are unrelated to the members of the current Board of Directors” (Arthur and Belinda Keiser, and James Waldman, an attorney who was then vice mayor of Coconut Creek).

Eventually, on July 7, 2002, the IRS relented and granted Everglades College tax-exempt status, saying to Keiser, “assuming your operations will be as stated in your application for recognition of exemption.” As Table 2 shows, this conditions appears not to have been met.

Table 2

The spirit of nonprofit governance by an independent board of trustees appears to be severely strained in the case of Everglades College. According to records available from the Florida Division of Corporations, at the time that Dale Chynoweth was added to the board of directors, he was hardly “unrelated” to other board members, as he was partner with Arthur Keiser in at least one business (Spectrum Business Park Association). In the ensuing years, the two were business partners in multiple properties that are rented by Everglades College. Zev Helfer joined Arthur Keiser as a business partner (College Pathology Labs, Inc.) just months before being named as an added “unrelated” director of Everglades College, Inc. James Waldman became a state representative, is the general counsel of Everglades College, Inc., and is the registered agent for various related Keiser businesses.

In addition to a board of directors, the corporate bylaws submitted to the IRS for Everglades College, Inc., call for a separate board of trustees to run the college. The bylaws declared that “The independence of the Board of Trustees is crucial to ensure that Everglades College meets the needs of the communities in which it serves,” and Everglades told the IRS that no more than two trustees would either be employees or have “any other business relationship with Everglades College.” The 2011 Form 990 submitted to the IRS for Everglades College indicates that three of the trustees owned businesses involved in transactions with Everglades College.

The Form 990 for 2011 also revealed that Everglades College had purchased the schools owned by the Keiser family, valued at $521,379,055, with $300,000,000 paid through a loan from the Keisers themselves and the remainder considered a tax-deductible donation by the Keisers. In total, the 2011 Form 990 reveals that Everglades College, Inc., paid $34,481,789 to entities owned by Keiser family members, including:

- $10,875,079 pursuant to the purchase agreement for the Keiser schools;

- $21,205,015 in rent and hotel stays at properties owned at least in part by the Keisers;

- $1,449,086 for chartered plane travel through companies at least partly owned by the Keisers; and

- $130,305 for services from a computer company owned by Keiser family members

To provide some perspective on the enormity of the $34 million total, consider that the highest-paid nonprofit president as reported by the Chronicle of Higher Education for 2012 earned $7 million,33 and the $34 million would cover the combined salaries of all of the top forty highest-paid public university presidents in 2013.34Arthur Keiser told a reporter that selling his Keiser schools to Everglades was about “ensuring his family would have a continuing role in running the university.”35

Offered the opportunity to comment on a summary of these findings, a representative of Keiser University provided a brief statement describing the school’s history and asserting that “The structure of the corporation and acquiring of assets followed ALL state and federal guidelines and regulations.”

Source Documents for Everglades College

- IRS Denial of Tax Exemption (undated, est. 2000)

- September 2000 Form 1023 and related materials [Application for Recognition of Exemption under Section 501 (c)(3)]

- IRS Request for Additional Information I (December 1, 2000)

- Everglades Response I (March 30, 2001)

- IRS Request for Additional Information II (May 3, 2001)

- Everglades Response II (May 21, 2001)

- IRS Request for Additional Information III (June 7, 2001)

- Everglades Response III (June 19, 2001)

- IRS Request for Additional Information IV (June 26, 2001)

- Everglades Response IV (July 10, 2001)

- IRS Letter Closing Case for Lack of Necessary Information (July 16, 2001)

- IRS Explanation of Problems with Everglades Application (December 18, 2001)

- Everglades Responds, Requesting Reconsideration (January 2, 2002)

- IRS Request for Additional Information V (February 16, 2002)

- Everglades Response V (March 8, 2002)

- IRS Response (April 9, 2002)

- Everglades Response VI (April 29, 2002)

- IRS Determination Letter (June 7, 2002)

- College Pathology Labs, Inc., Articles of Incorporation (2001) [acquired through Florida Secretary of State]

- Spectrum Business Park Association, Inc., Corporate UBR Filing (2001) [acquired through Florida Secretary of State]

- 2011 Form 990

- 2012 Form 990

- 2013 Form 990

Center for Excellence in Higher Education

DBA Stevens-Henager College, CollegeAmerica AZ, California College San Diego, and CollegeAmerica Colorado/Wyoming

On March 1, 2013, the IRS received a Form 8940 “Request for Miscellaneous Determination” from a small organization, the Center for Excellence in Higher Education (CEHE), which had originally been incorporated in Indiana in 2006. CEHE asked the IRS to approve the organization’s shift from being considered tax-exempt as a charity to being considered tax-exempt as an educational organization. The law firm submitting the request explained that the change was being requested because CEHE had acquired a set of for-profit colleges owned by Carl Barney or by trusts of which he is the sole beneficiary.

The materials submitted to the IRS describing the organizational changes that were involved in the purchase of Carl Barney’s colleges run more than five hundred pages. Within the IRS documents examined for this report, there is no indication that the IRS has verified that the purchased colleges are following the rules of nonprofit governance. The colleges, nonetheless, now describe themselves as dedicated to putting students first because they are nonprofit. Carl Barney’s colleges were valued at $636,147,213 for the purposes of the purchase by CEHE. Of this amount, $431 million was incorporated into interest-bearing notes committing CEHE to pay Barney over time, and the remaining $205 million was considered a tax-deductible contribution from Barney to the nonprofit.

As part of the transaction, Barney became the “sole member” of the CEHE corporate entity, with “the right, inter vivos or by testament, to transfer such membership to another person,” according to the CEHE’s revised articles of incorporation. The revised bylaws state further that Barney, as the sole member, had the authority to name and remove board members. In other words, Carl Barney, who is owed $431 million by CEHE, fully controlled the supposedly nonprofit CEHE. On September 16, 2015, Barney filed a change in the CEHE articles of incorporation with Indiana secretary of state adding two additional members: Peter LePort and C. Bradley Thompson.

The various campuses owned by CEHE earn revenue of about $200 million per year, largely from federal programs that are funded by U.S. taxpayers. The various schools run by CEHE have recently come under fire. In 2014, the U.S. Department of Justice joined in a lawsuit against Stevens-Henager College, alleging that the school was using improper bonuses to pay its recruiters.36 In December 2014, Colorado officials sued CollegeAmerica over misleading advertising.37 In June 2015, several CollegeAmerica schools were placed on probation by their accreditor, based on concerns about low job placement rates.38 And as of September 9, 2015, the Department of Education considers CEHE’s request to be considered a nonprofit an open case “undergoing substantive review.”39

Is the $636 million a fair price for Barney’s colleges? In response to a request for comment, a CEHE official told The Century Foundation that the amount was reviewed by an independent valuation consultant and that the prior board of CEHE were not paid in the sale. Yet according to the organization’s financial statements, the bulk of the price, $419 million, was not for tangible assets, but instead for the colleges’ supposedly valuable reputations (accountants apply the term “goodwill” to the difference between a business’s purchase price and the fair market value of the tangible assets). In other words, Barney is being paid and claiming a tax deduction for CEHE acquiring the reputations of colleges that are currently the subjects of multiple government investigations.

According to the organization’s Form 990 for 2013, the eleven-member board of CEHE, only two of whom are uncompensated, paid Barney, the chairman of the board, more than $16 million that year: $11,231,444 of the purchase price with interest, $5,097,509 for property leases, and a small salary.

Source Documents for Center for Excellence in Higher Education

- February 2013 Form 1023 and related materials [Application for Recognition of Exemption under Section 501 (c)(3)]

- 2012 Audit Report

- Amendment to the Articles of Incorporation of CEHE

- 2012 Form 990

- 2013 Form 990

The Cost of the Subterfuge

Covert for-profit colleges cost the public by misleading consumers, dodging taxes, and evading regulations that apply to Education Department financial aid. Further, their actions, and the failure of the federal government to address the problem, seriously undermine the integrity of the system of oversight of colleges and universities, as well as of charitable organizations as a whole.

Shortchanging Consumers

Colleges emphasize that they are public or nonprofit because these labels mean something. The labels certify that everything the college does, including how it spends its money, is overseen by trustees who are not seeking personal financial gain. They are vouching for the institution, and they affirm that there are valid educational or other charitable purposes behind every penny spent by the institution.

Placing ultimate control of colleges in the hands of people who do not have a conflict of interest produces better overall outcomes for students and society. For-profit colleges charge higher prices to the neediest students, have higher dropout rates, yield lower earnings for their graduates, and their students have greater difficulty repaying their student loans. In addition, for-profit colleges divert much of their tuition revenue to profit and marketing rather than education. At more than nine out of ten nonprofit institutions, the proportion of tuition revenue that is spent on instruction (actual teaching by faculty) is at least 50 percent. The schools examined in this report all fall far below that mark. Herzing was the highest at 39 percent, with Everglades/Keiser at 31 percent, Remington at 31 percent, and Carl Barney’s school’s spending only 16 percent of tuition revenue on instruction.40

Much of what matters most in education, however, is difficult if not impossible to quantify and measure because it involves the unknown potential futures of students. Colleges operate as nonprofit or public entities to prevent students’ futures from being sacrificed to enrich an investor who wants a bigger, faster financial return. Operating as a nonprofit does not guarantee that students are treated well, but it increases their chances by eliminating owner and investor pressures.

All four of the colleges in this report are using their claim to nonprofit status as a marketing tool. But if they are not actually controlled by financially disinterested boards, then that layer of consumer protection is absent, and consumers are being misled.

Hiding from Regulations

As described earlier in this report, for-profit colleges are allowed access to federal financial aid only under particular circumstances. First, for-profit schools must meet a market test, demonstrating that a portion of their revenue comes from somewhere other than federal aid. Even though this requirement has serious loopholes, many for-profit colleges still come very close to transgressing the 90 percent limit on Department of Education revenue, so the threshold is a serious concern that could motivate schools to seek nonprofit status. And in fact, as noted earlier, Remington was quite open that the 90–10 rule was an impetus for seeking to be considered nonprofit.

Second, programs at for-profit institutions are eligible for Department of Education aid only if they are focused on training for a job, leading to gainful employment. They are not eligible to receive federal funding for programs that focus on less tangible benefits, such as intellectual enrichment—only public and nonprofit institutions are trusted to receive public funding to offer degrees involving broader, less measurable goals.

Covert for-profit colleges that obtain paperwork identifying them as nonprofit institutions, yet fail to follow nonprofit governance structures, are evading these regulatory structures.

The colleges examined for this report have in recent years received a total of more than half a billion dollars every year in Pell Grants and students loans from the Department of Education. They also take in additional funds from other federal and state agencies, as well as additional tuition payments from students and their families.

If the colleges are not truly the nonprofit entities they claim to be, then many of these funds are being claimed inappropriately.

Evading Taxes

While the consumer protection offered by non-owner control is the most critical issue at play, there are two ways that tax laws treat nonprofits differently from for-profit entities. One is that donations to nonprofits can be deducted from the donor’s income, reducing his income tax liability. This is a gain that comes not to the college but to the individual making the donation—though obviously the deductibility also helps the institution’s fundraising. At least two of the conversions described in this report involved transactions in which the purchasing nonprofit gave the sellers credit for a “donated” portion of the sale price. If the deductions were taken by the sellers involved in the CEHE and Everglades transactions, the forgone federal income tax revenue could total more than $100 million.

The other benefit afforded nonprofit institutions is that their net income—revenue they decide to hold for future charitable purposes—is not subject to corporate income taxes. If the entities examined for this report ultimately have their nonprofit status revoked retroactively, then they will owe back taxes on the net income for every year that nonprofit status was inappropriately claimed. Based on the tax returns examined for this report, this liability could run into the hundreds of millions of dollars.

What Should Happen Now

The four examples of covert for-profit colleges examined in this report should be enough to suggest swift and decisive action by regulatory agencies. The potential for a flood of conversion efforts makes attention to this issue all the more urgent: As recently as June, a lawyer involved in CEHE’s purchase of Carl Barney’s schools was being touted by his firm as an expert who can help other for-profit colleges avoid regulations and taxes by converting to nonprofit status.41 With the gainful employment rule having taken effect in July 2015, more for-profit colleges may search for a way to dodge the requirement rather than comply. Indeed, on an investor call in November 2014, executives of one publicly traded company downplayed the coming regulations, explaining that they had options available, including “organizational structural changes, such as moving to a nonprofit model. . . . [W]e currently have a nonprofit entity that could be used in such a transaction.”42

What follows are recommendations for both the IRS and the Department of Education.

IRS Monitoring and Enforcement

The problem of inadequate oversight of charities by the Exempt Organizations Division of the IRS (caused in part by inadequate funding of the IRS) has been a focus of congressional attention and a recent report by the Government Accountability Office.43 Among other things, the IRS has committed to refining its targeting of reviews of existing nonprofits so that the most significant hazards are more likely to be addressed in a timely manner. The plans do not go far enough, however, because they take into consideration only the IRS’s priorities rather than the interests of other federal agencies that rely on IRS determinations. The issue is not just about charities’ assertions that donations will be tax deductible, but also the cascade of events that follows such a determination: the public funding that will be going to the institutions, and students and families taking out student loans and committing time and energy to an education that is not what was advertised.

Because the IRS handles tax documents, it is particularly attuned to issues of privacy. But the work of the Exempt Organizations Division is different because nonprofit organizations are required to have some degree of transparency. Particularly when the tax-exempt status of these organizations opens the door to federal funding, the IRS should work hand-in-hand with the relevant federal agencies to make sure that its determinations about organizations’ nonprofit status are accurate, valid, and current, based on information available from all sources.

Education Department Monitoring and Enforcement

It is problematic that the Department of Education has been relying solely on IRS letters to determine a college’s eligibility for federal financial aid. The agency’s own regulations call for a more rigorous review, requiring colleges that wish to be treated as nonprofit to show, in addition to the IRS designation, that “no part of the net earnings” of the school “benefits any private shareholder or individual,” and that the school is authorized as a nonprofit institution by the states in which it operates.44

With this in mind, the secretary of education should immediately:

- Aggressively review recent nonprofit conversions to determine regulatory compliance.

- Place a moratorium on Department of Education approval of any additional institutions seeking to be treated as nonprofit.

- Revise the documentation and assertions required of institutions claiming nonprofit status.

- Seek the assistance of states and accreditors to identify any institutions that are claiming to be nonprofit but may be operating in a manner that inappropriately benefits an individual or shareholder.

During the moratorium, the Department of Education and the IRS should develop a joint work plan for the review of nonprofit institutions going forward. The application for access to federal aid (program participation agreement) should require all institutions to attest they are in full compliance with IRS and Department of Education rules regarding nonprofit operations. Internal conflicts of interest and changes in governance should be fully assessed before federal aid is made available to an institution. Finally, any proposed change of ownership involving a nonprofit institution should be subject to public review prior to approval by the department.

It is clear that the 90–10 rule, which applies only to for-profit colleges, is one reason that for-profit college owners are now seeking ways to cloak themselves as nonprofit. In addition to examining more closely any nonprofit conversions, the Department of Education should also monitor for-profit institutions’ relationships with scholarship entities to prevent their inappropriate use in the 90–10 calculations. If the 10 percent portion in the 90–10 rule is achieved with funds controlled, directly or indirectly, by the for-profit—such as through an affiliated nonprofit scholarship fund—then the market accountability mechanism is undermined. In addition, Congress may want to consider applying an improved version of the 90–10 rule more broadly. While nonprofit and public institutions typically have far fewer than 90 percent of their students using federal aid, some do price some programs to take maximum advantage of the federal aid that is available. Requiring some market price accountability in those situations is worth considering.

Longer term, the Department of Education should consider whether the determination of a school’s eligibility is well placed in its current location at Federal Student Aid (FSA). FSA’s primary task is operational, processing millions of FAFSAs and millions of grant and loan payments. The role of policing schools might be carried out more effectively if it was placed at an enforcement entity, such as the Office of Inspector General. While care should be taken not to expect too much from moving organizational boxes, this may be one case where there could be real benefits. The White House might even consider the idea of linking the school eligibility roles of the Departments of Education, Veterans Affairs, Defense, and Labor.

Notes

-

1. See Committee on Health, Education, Labor, and Pensions, United States Senate,

For Profit Higher Education: The Failure to Safeguard the Federal Investment and Ensure Student Success

(Washington, D.C.: Government Printing Office, July 30, 2012),

http://www.gpo.gov/fdsys/pkg/CPRT-112SPRT74931/pdf/CPRT-112SPRT74931.pdf

2. National Center on Education Statistics, “Undergraduate Enrollment,” http://nces.ed.gov/programs/coe/indicator_cha.asp, accessed August 31, 2015.

3. U.S. Department of Education, “Obama Administration Takes Action to Protect Americans from Predatory, Poor-Performing Career Colleges,” March 14, 2014, http://www.ed.gov/news/press-releases/obama-administration-takes-action-protect-americans-predatory-poor-performing-career-colleges.

4. Alia Wong, “The Downfall of For-profit Colleges,” Atlantic, February 23, 2015, http://www.theatlantic.com/education/archive/2015/02/the-downfall-of-for-profit-colleges/385810/.

5. The requirement that nonprofits reinvest rather than distribute profits is known as a “nondistribution constraint.” Henry B. Hansmann, “The Role of Nonprofit Enterprise,” Yale Law Journal 89, no. 5 (1980): 835–901.

6. Michael Johnston, “Wikipedia Revenue Analysis: How a Wiki Could Make $2.8B a Year,” MonetizePros blog, http://monetizepros.com/blog/2013/analysis-how-wikipedia-could-make-2-8-billion-in-annual-revenue/. In comparison, Wikimedia’s Form 990 shows revenue of $45 million.

7. Helmut K. Anheier and Jeremy Kendall, “Trust and voluntary organisations: Three theoretical approaches,” Working Paper 5, Centre for Civil Society, 2000, http://eprints.lse.ac.uk/29035/.

8. Glenn C. Altschuler and Stuart M. Blumin, The GI Bill: A New Deal for Veterans (New York: Oxford University Press, 2009).

9. The 85-15 rule is discussed in a Supreme Court ruling that upheld it, Cleland v. National Coll. of Business, 435 U.S. 213 (1978), https://supreme.justia.com/cases/federal/us/435/213/case.html. For a discussion of more recent versions of the rule see Robert Shireman, “Behind the Fraud Charges against ITT Education,” Huffington Post, May 13, 2015, http://www.huffingtonpost.com/robert-shireman/behind-the-stock-fraud-ch_b_7271134.html.

10. The National Defense Education Act of 1959 defined an eligible institution of higher education as one that is, among other things, a “public or other nonprofit institution.” The National Defense Education Act of 1959, Public Law 85-864, U.S. Statutes at Large 72 (September 2, 1958), http://www.gpo.gov/fdsys/pkg/STATUTE-72/pdf/STATUTE-72-Pg1580.pdf.

11. Higher Education Act of 1965, Public Law 89-329, 89th Cong. 1st sess. (Government Printing Office, 1965), https://bulk.resource.org/gao.gov/89-329/00004C64.pdf.

12. See the history included in the proposed regulation. Department of Education, “Program Integrity: Gainful Employment; Proposed Rule,” Federal Register 79 (57) (2014): 16426–643, http://www.gpo.gov/fdsys/pkg/FR-2014-03-25/pdf/2014-06000.pdf.

13. Robert Rothman, “Bennett Asks Congress to Put Curbs on ‘Exploitative’ For-Profit Schools,” Education Week, February 17, 1988, http://www.edweek.org/ew/articles/1988/02/17/07450039.h07.html. And American Council on Education, “Bennett Cites Abuses, Defaults at Proprietary Schools ,” Higher Education and National Affairs, February 15, 1988.

14. For more information about the gainful employment rule, which took effect on July 1, 2015, see “Gainful Employment Rule Questions & Answers,” Protect Students and Taxpayers website, June 30, 2015, http://www.protectstudentsandtaxpayers.org/wp-content/uploads/2015/06/GainfulEmploymentQA_June-30-2015-_5-pages.pdf.

15.See Career Education Corporation earnings call, November 6, 2014, and Ronald J. Hansen, “GCU Non-profit Would Break New Ground, Enrich Execs,” Arizona Republic, January 26, 2015, http://www.azcentral.com/story/money/business/2015/01/17/gcu-non-profit-break-new-ground-enrich-execs/21942343/.<br>

16. Technically, an entity organizes itself as a nonprofit under state law, and seeks from the IRS the additional designation of being a “tax-exempt” nonprofit, one that is not subject to corporate income taxes (because it will be reinvesting its earnings into charitable purposes). Depending on the type of IRS approval, donors may also be able to deduct their contributions from personal income taxes.

17. 26 CFR 601.201(n)(3)(ii).

18. CFR 601.201(n)(6)(i) and (vii).

19. Partners in Charity, Inc. v. Commissioner 141 T.C. 151, 141 T.C. No. 2 (2013).

20. U.S. Government Accountability Office, “Tax-Exempt Organizations: Better Compliance Indicators and Data, and More Collaboration with State Regulators Would Strengthen Oversight of Charitable Organizations,” December 2014, http://www.gao.gov/assets/670/667595.pdf.

21. Author’s communication with staff of the U.S. Department of Education, including a discussion with the Office of the Undersecretary on June 1, 2015.

22. Committee on Health, Education, Labor, and Pensions, United States Senate, For Profit Higher Education.

23. Revenue and 90–10 figures were provided by Herzing University in response to a request for comment.

24. Rick Romell, “Herzing University becomes a nonprofit organization,” Milwaukee Journal-Sentinel, January 2, 2015, http://www.jsonline.com/business/herzing-university-becomes-a-nonprofit-organization-b99419151z1-287365131.html.

25. Letter from Ted Mitchell, undersecretary of education, to Representative Rosa L. DeLauro, September 9, 2015, on file with the author.

26. Goldie Blumenstyk, “Another College Takes the Path From For-Profit to Nonprofit,” Chronicle of Higher Education, January 20, 2011.

27. See report on Education America (Remington) in Committee on Health, Education, Labor, and Pensions, United States Senate, For Profit Higher Education.

28. See discussion on page 96 of the application for tax-exempt status.

29. See section XXI of the Stephens Retirement Services “Investment Management and Plan Services Agreement,” at pages 128-9 of Remington’s Form 1023 source document, available online.

30. The revised bylaws give the “sole member” of Remington Colleges, Inc., the authority replace trustees.; The sole member is Warren Stephens, through his effective control of The Stephens Charitable Trust. See page 70 of Remington’s Form 1023: “The sole member of the College is the Jackson T. Stephens Charitable Trust (the “Trust”), a Sec. 501 (c)(3) organization. Warren Stephens, a member of the Board, is a trustee of, and effectively controls, the Trust.”

31. See 2010 Form 1023 in Remington source documents, available online.

32. International Postgraduate Medical Foundation v. Commissioner, 56 T.C.M. 1140 (1989).

33. See Shirley Ann Jackson at Rensselaer Polytechnic Institute, in “Executive Compensation at Public and Private Colleges,” database at The Chronicle of Higher Education (paywall), http://chronicle.com/factfile/ec-2015/#id=18461_194824_2012_private.

34. “Compensation of Chief Executives at Public Colleges, 2013-13,” Chronicle of Higher Education, June 12, 2015, A31.

35. Paul Fain, “Dropping Profit,” InsideHigherEd, July 17, 2014, https://www.insidehighered.com/news/2014/07/17/few-profits-have-become-nonprofits-despite-regulatory-environment.

36. David Halperin, “Justice Department Sues For-Profit Stevens-Henager College,” Huffington Post, June 9, 2014 (updated), http://www.huffingtonpost.com/davidhalperin/breaking-justice-dept-sue_b_5120249.html.

37. Kieran Nicholson, “CollegeAmerica sued by Colorado AG for ‘deceptive trade practices,” Denver Post, February 17, 2015, http://www.denverpost.com/news/ci_27544803/collegeamerica-sued-by-colorado-ag-deceptive-trade-practices.

38. Letters released by the Accrediting Commission of Career Schools and Colleges, June 17, 2015, http://www.accsc.org/UploadedDocuments/Commission%20Actions/Probation%20Summary%206-17-15.pdf.

39. Letter from Ted Mitchell, undersecretary of education, to Representative Rosa L. DeLauro.

40. Based on 2011 data reported by institutions to the Integrated Postsecondary Data System, National Center for Education Statistics. The ratio was determined by taking the enrollment-weighted average of individual campus data for each group of campuses.

41. An unsolicited e-mail from a Los Angeles law firm, sent to the Republic Report (which had written about the topic of conversions of for-profit colleges). A copy of the e-mail is available at TCF online https://www.dropbox.com/s/yyj0ousyuofq18r/Email%20sent%20to%20the%20Republic%20Report.pdf?dl=0.

42. Career Education Corp earnings call, November 6, 2014.

43. U.S. Government Accountability Office, “Tax-Exempt Organizations.”

44. 34 CFR 600.2.